Tips On Getting The Most Out Of Your Home Mortgage

Content author-Jimenez CrossMillions of people want to own a home. When one becomes a homeowner, there is a huge feeling of pride and accomplishment involved. Many people need a mortgage to help them purchase their home. There are several key facts to learn before getting a loan, and this article can be a great help.

Before beginning any home buying negotiation, get pre-approved for your home mortgage. That pre-approval will give you a lot better position in terms of the negotiation. It's a sign to the seller that you can afford the house and that the bank is already behind you in terms of the buy. It can make a serious difference.

Having the correct documentation is important before applying for a home mortgage. Before speaking to a lender, you'll want to have bank statements, income tax returns and W-2s, and at least your last two paycheck stubs. If you can, prepare these documents in electronic format for easy and quick transmission to the lender.

Like most people, you will likely have to have some amount of money for a down payment. Some banks used to allow no down payments, but now they typically require it. Consider your finances carefully and find out what kind of down payment you will need to provide.

Be prepared before obtaining your mortgage. Every lender will request certain documents when applying for a mortgage. Do not wait until they ask for it. Have the documents ready when you enter their office. You should have your last two pay stubs, bank statements, income-tax returns, and W-2s. Save all of these documents and any others that the lender needs in an electronic format, so that you are able to easily resend them if they get lost.

Avoid fudging the numbers on your loan application. It is not unusual for people to consider exaggerating their salary and other sources of income to qualify for a larger home loan. Unfortunately, this is considered froud. You can actually be criminally prosecuted, even though it doesn't seem like a big deal.

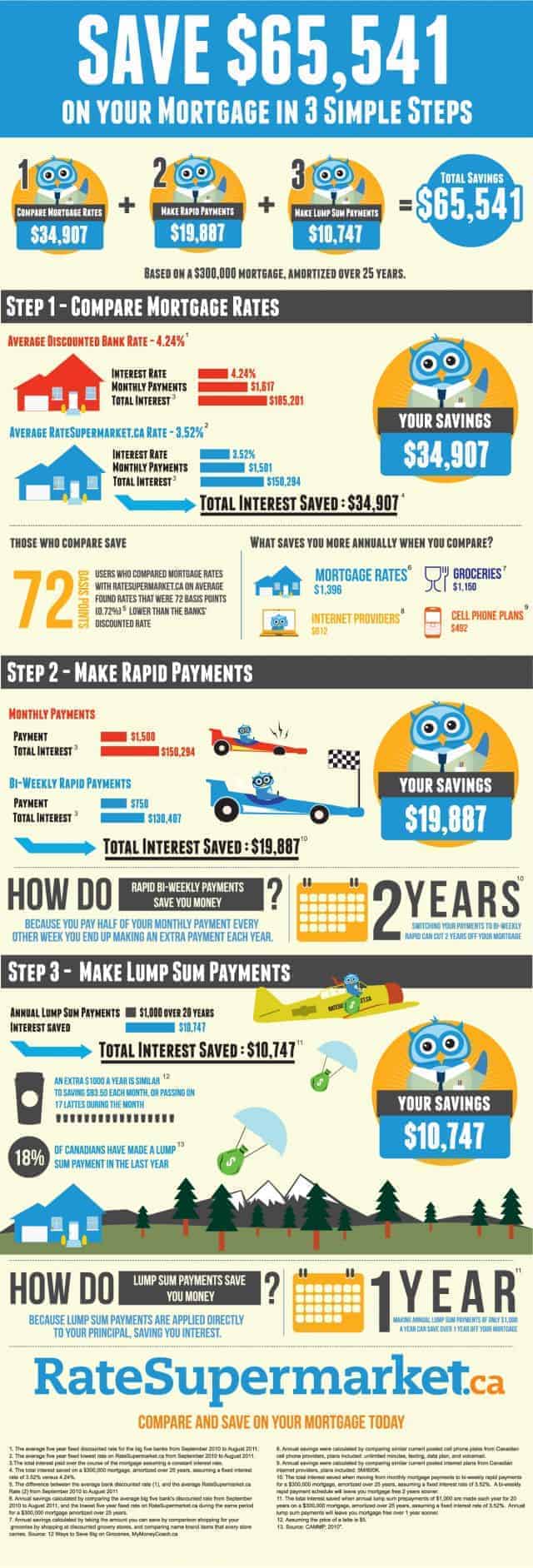

Locate the lowest rate for interest you can find. The bank is seeking the best way to get you locked in at an interest rate that is high. Avoid being the next person they sucker in. Give yourself several choices by looking at many offers from different lenders.

Consider having an escrow account tied to your loan. By including your property taxes and homeowners insurance into your loan, you can avoid large lump sum payments yearly. Including these two items in your mortgage will slightly raise the monthly payment; however, most people can afford this more than making a yearly tax and insurance payment.

Make sure you've got all of your paperwork in order before visiting your mortgage lender's office for your appointment. While logic would indicate that all you really need is proof of identification and income, they actually want to see everything pertaining to your finances going back for some time. look at this now is different, so ask in advance and be well prepared.

There are many different types of home mortgage loans available, and some are much easier to get than others. If you are having a problem getting a conventional loan, try applying for an adjustable rate mortgage or a balloon. These are short term loans ranging from one to 10 years, and need to be converted when they expire.

Don't use real estate brokers or mortgage lenders who encourage you to lie on your home mortgage application. It is illegal to lie on this application, and it is a legal document. Misrepresenting your income or other information is grounds for criminal prosecution. Working with people who encourage you do commit a crime is not a good idea.

Current interest rates on home mortgages are lower than they have been in years. Experts expect them to begin increasing again shortly, so now is a great time to purchase a home and finance it at a low rate. The shorter the term of the mortgage, the better the rate you will be able to get.

If you are looking to buy any big ticket items, make sure that you wait until your loan has been closed. Buying large items may give the lender the idea that you are irresponsible and/or overextending yourself and they may worry about your ability to pay them back the money you are trying to borrow.

Do not give up if you do not have success getting a home mortgage. Do what you have to do to change your credit score, save some more money or whatever else you have to do to get yourself in a home. Don't, however, sign up for a mortgage that you will have trouble paying.

It is very important to have adequate savings before considering buying a home. You are going to need money to cover the down payment, closing costs and other things like the inspection, fees for applications and appraisals. If you have a large down payment, you will have a better mortgage.

Answer every question on your home mortgage application absolutely honestly. There is no benefit in lying, as all of the information that you provide will be thoroughly examined for accuracy. Additionally, a small fib could easily lead to your denial, so just be honest from the start so that you have the best chances.

Take note of home buying season. Usually markets will have hot and cold selling periods. The hotter the selling period, the more shady lenders are likely to be around. If you know what trend the market is in, you will better be able to guard against people looking to take advantage of you.

There are times when the seller of a home will be able to give you a land contract so you can purchase the home. The seller needs to own the home outright, or owe very little on it for this to work. Read More Listed here may need to be paid within a few years.

Now that you know what it takes to get a mortgage which fits your needs, you have to get down to work and do it. Follow the steps laid out here and begin your planning process. Soon enough, you'll find a great lender who is offering a great rate and your job will be done.